Interest overview

Credit card APR is an annual rate that represents the cost of borrowing money on a credit card. For a quick estimate, this calculator converts APR from a percentage to a decimal, divides it by 365 to get a daily periodic rate, multiplies that daily rate by the carried balance, and then multiplies the daily interest by the days remaining before the selected billing cycle close. This method is widely used because credit card interest accrues daily rather than monthly, making the daily periodic rate the most practical way to estimate interest charges between statement dates.

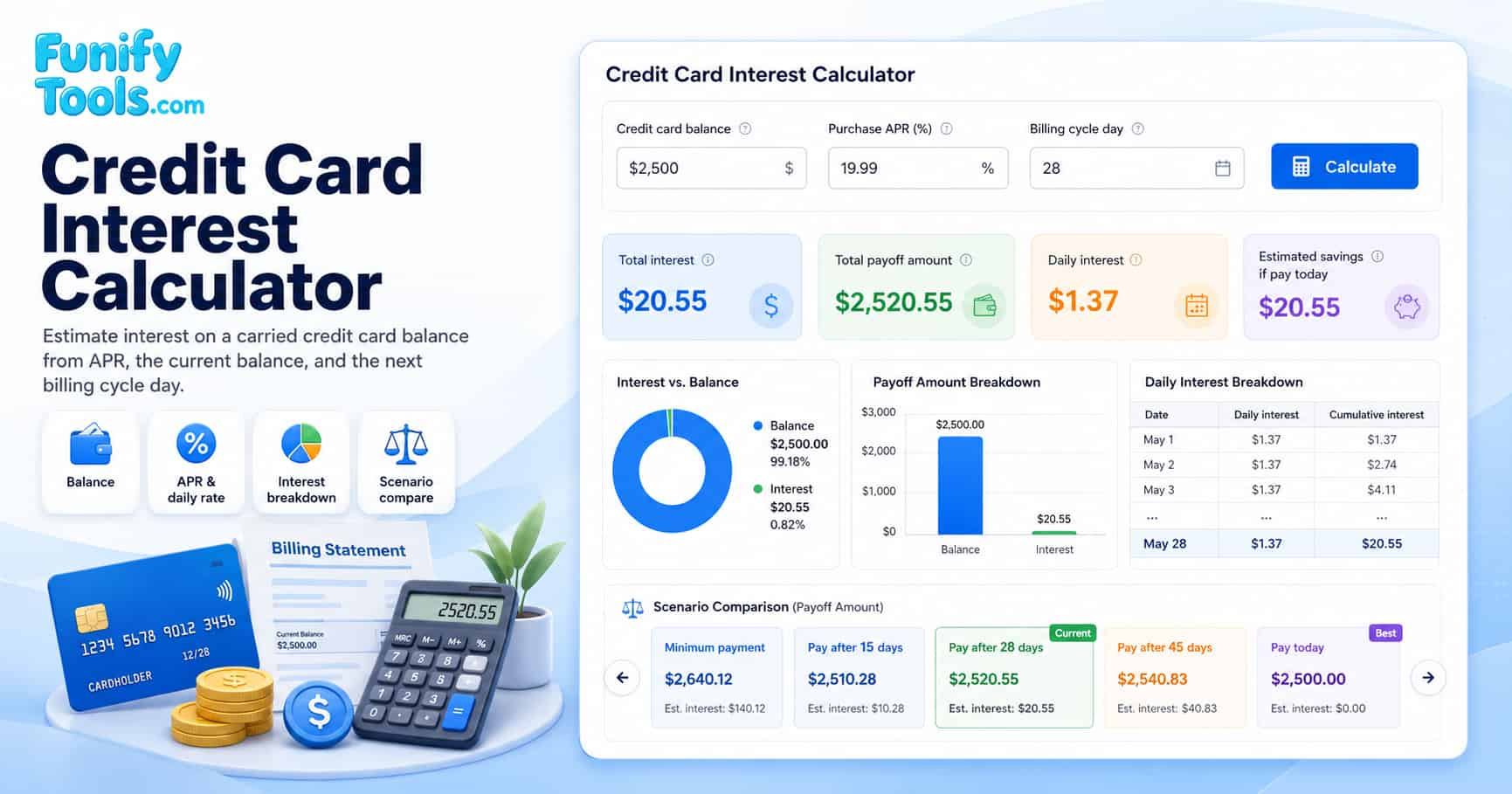

A credit card interest calculator is helpful when you carry a balance and want to estimate the cost of waiting until the next billing cycle close. It is especially useful for comparing a current payoff against paying later, because credit card interest is usually tied to time, balance, and APR rather than a fixed monthly fee. Understanding how much interest accumulates each day can help you make informed financial decisions about when to pay down your balance.

If you want broader background, search Google for how credit card interest is calculated APR daily periodic rate. Issuer terms can vary, but the daily periodic rate is a common way to explain purchase interest across most major card networks including Visa, Mastercard, and American Express.

APR and daily periodic rate

Daily rate = (APR / 100) / 365

Daily interest = balance x daily rate

Payoff = balance + estimated interest

APR is quoted annually, but most quick credit card interest estimates convert it into a daily rate. For example, a 24.99% purchase APR becomes a much smaller daily percentage, but that small daily charge can add up when the balance remains unpaid for many days. Over a full 30-day billing cycle, a $2,500 balance at 24.99% APR would accrue approximately $51.35 in interest under the constant balance assumption.

Some issuers use average daily balance methods, compounding, promotional APRs, cash advance APRs, or separate rates for purchases and transfers. If those terms are relevant, search Google for average daily balance method credit card interest explained before comparing this simplified estimate with a statement. Understanding the difference between purchase APR, balance transfer APR, and cash advance APR is essential for accurately estimating total credit card costs.

Billing cycle notes

If today is already past the billing cycle day you enter, the calculator moves the estimate to that day in the next month. When a month has fewer days than the entered billing day, the calculator uses the last valid day of that month. This behavior ensures that the estimate always reflects a forward-looking billing period regardless of when you use the tool.

The billing cycle day is not always the payment due date. The cycle close date usually determines the statement period, while the due date is later. Interest rules can depend on whether a balance was carried from a previous statement, whether the full statement balance was paid, and whether new purchases still qualify for a grace period. Most credit card issuers offer a grace period of at least 21 days between the statement closing date and the payment due date, during which no interest is charged if the full balance is paid.

| Days remaining in cycle | Estimated interest on $2,500 at 24.99% APR | Payoff total estimate |

|---|---|---|

| 5 days | $8.56 | $2,508.56 |

| 10 days | $17.12 | $2,517.12 |

| 15 days | $25.67 | $2,525.67 |

| 20 days | $34.23 | $2,534.23 |

| 25 days | $42.79 | $2,542.79 |

| 30 days | $51.35 | $2,551.35 |

Early payment view

The savings estimate shows the interest that may be avoided by paying now instead of waiting until the calculated cycle close date, assuming the balance would otherwise stay unchanged. This is one of the most practical features of the credit card interest calculator because it directly answers the question: how much money can I save by paying my balance early?

This makes the calculator useful for everyday decisions: comparing a payoff today, waiting for payday, or making a partial plan around a cycle close. A larger balance, higher APR, or longer wait creates a larger estimated interest cost. The earlier you pay down a carried balance, the fewer days of daily periodic rate accumulation you incur, which directly reduces the total interest charged on your account.

Interest scenarios by balance and APR

The table below shows how different combinations of balance and APR affect the estimated monthly credit card interest over a typical 30-day billing cycle. This can help you compare your current situation with potential changes in your balance or APR.

| Balance | 15% APR (30-day interest) | 20% APR (30-day interest) | 25% APR (30-day interest) | 29.99% APR (30-day interest) |

|---|---|---|---|---|

| $1,000 | $12.33 | $16.44 | $20.55 | $24.65 |

| $2,500 | $30.82 | $41.10 | $51.37 | $61.62 |

| $5,000 | $61.64 | $82.19 | $102.74 | $123.25 |

| $10,000 | $123.29 | $164.38 | $205.48 | $246.49 |

As the table demonstrates, higher APRs have a compounding effect on larger balances. If you are carrying a balance across multiple cards, paying off the card with the highest APR first can yield the greatest interest savings. For more information on prioritizing credit card payments, search Google for credit card payoff strategy high APR interest savings and compare the effect of paying high-APR balances first.

| Term | Definition | Impact on your interest |

|---|---|---|

| APR (Annual Percentage Rate) | The yearly interest rate charged on credit card balances, expressed as a percentage. | A higher APR directly increases the daily periodic rate and total interest charged over time. |

| Daily periodic rate (DPR) | APR divided by 365, representing the interest rate applied to the balance each day. | DPR determines how much interest accrues per day; even a small DPR adds up over a full billing cycle. |

| Average daily balance | The sum of each day's balance during a billing cycle divided by the number of days in the cycle. | Many issuers use this method to calculate interest; making a mid-cycle payment reduces the average daily balance. |

| Grace period | The time between the statement closing date and the payment due date when no interest is charged on new purchases if the previous balance was paid in full. | Paying the full statement balance by the due date allows you to avoid interest charges entirely during the grace period. |

| Minimum payment | The smallest amount you must pay each month to keep the account in good standing, typically 1-3% of the balance plus interest and fees. | Paying only the minimum extends the repayment period significantly and increases total interest paid over the life of the debt. |

Assumptions and limits

This calculator assumes the balance stays constant from today through the selected billing date. Purchases, payments, refunds, cash advances, annual fees, late fees, promotional rates, and issuer rounding rules can all change actual credit card interest. The estimate is designed for educational and planning purposes rather than as a substitute for an official statement from your card issuer.

The result is not a statement payoff quote. For a real payoff amount, use your issuer account page or contact the card issuer directly. If you are reviewing debt payoff strategies, search Google for credit card debt repayment strategy reduce interest charges to explore approaches such as the debt avalanche method, debt snowball method, or balance transfer options that can help lower your overall interest burden.

References

Consumer Financial Protection Bureau: Credit cards - Official U.S. government resource for understanding credit card terms, rights, and consumer protections.